Protecting Your Home Head to Toe: Understanding Florida Peninsula’s Insurance Policy Coverage A to E

Do you remember the preschool song “Head, Shoulders, Knees, and Toes”?

The lyrics go like this:

Head, shoulders, knees and toes, knees, and toes.

Head, shoulders, knees and toes, knees, and toes.

And eyes and ears and mouth and nose.

Head, shoulders, knees and toes, knees, and toes.

All the parts named in this childhood song are pieces of a group-the body. When naming all of them you form the whole unit. This is the same way you can use in deciphering your home insurance coverages. Your home insurance policy consists of several coverages which may assist in paying to repair or replace your home and belongings should a covered peril cause damage or destroy them.

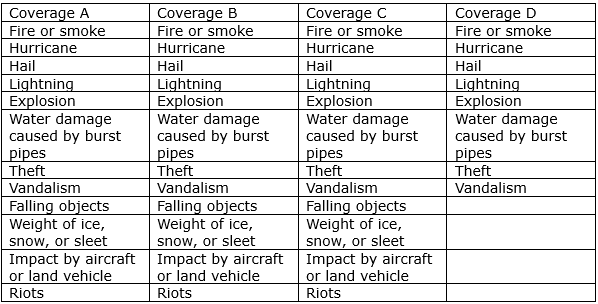

Peril definition. Perils typically covered by a standard home insurance policy include fire, wind, lightning, hail, vandalism, and theft.

Homeowners Insurance is something all Florida homeowners should consider and understand. If you are looking for coverage or upgrading your current policy, take a look at our coverage breakdown explaining the basics of each type of coverage.

Covering You and Your Home from Top to Bottom

Coverage A: The Head- The Physical Structure of the Home- Dwelling

Like the preschool song, we will start with the head first. Coverage A, or dwelling coverage, covers the main physical structure of the home. It is the most important part to be protected. It covers most instances of damage or destruction to your house or attached structures such as a garage or an addition.

While there are some rare cases where certain damages may be excluded from your insurance policy, you can rest assured knowing most home repairs and rebuilding costs will be paid by your dwelling coverage for all covered incidents.

Coverage B: The Shoulders- The Support to the Head- Other Structures

Usually found on the second line item on your policy declarations page of your homeowners policy, just like shoulders are after the head in the song, Coverage B covers Other Structures. Other Structures coverage protects physical structures, such as a shed or fence, which are on your property and not attached to your home. This coverage is the support to the main structure of your home, and it pays for replacement or repairs when these structures are affected by a covered peril.

What Other Structures are Covered under Coverage B?

A standard Florida Peninsula policy defines Coverage B as: “Other structures on the "residence premises" set apart from the dwelling by clear space.

These structures include:

- Fences

- Walls

- Sheds

- Swimming pools

- Detached garages/carports

Screen enclosure coverage is not always an industry standard, but an added benefit to our Florida Peninsula policyholders.

Coverage C: The Knees- Contents of the Home- Personal Property

We have talked about the head (Dwelling, Coverage A), shoulders (Other Structures, Coverage B), now we will address the knees- the actual contents of your house. Coverage C’s coverage includes furniture, clothing, jewelry, electronics, and appliances, if they are stolen, damaged, or destroyed. Personal property insurance covers the items inside the home, the prized possessions most important to you.

Coverage D: The Toes- Keeping You Moving Forward

Coverage D, or Loss of Use Coverage, kicks in should your main home be impacted by enough damage deeming your house inhabitable due to a covered loss. Should this unfortunate event happen, homeowners will need to find a new place to live, for a matter of days up to several months. Coverage D pays for additional living expenses as well as smaller expenses such as buying groceries, ordering food for takeout, moving expenses, storage fees, and transportation fees. With the help of Coverage D, or loss of use coverage, Florida Peninsula covers the costs associated with helping homeowners remain on their feet while their home is being rebuilt.

Coverage E: Eyes and Ears and Mouth and Nose- Personal Liability

Coverage E, or Personal Liability Coverage, protects your financial assets in the event of a potential lawsuit. Personal Liability Coverage covers things like medical bills, property repair, and legal fees if someone happens to be injured on your property.

Head, Shoulders, Knees, and Toes - What Peril is Covered?

How Much Coverage Do I Need?

There is a whole lot of mathing involved and it can seem very overwhelming. Your agent will be able to break down each section into detailed coverage amounts and help you do a full assessment but here is a quick digestible breakdown.

Coverage A (Dwelling): is determined by the cost to rebuild the home at today’s prices in the event of a covered loss. Factors such as building cost, materials, and labor factor into the Coverage A limit at the time the policy is purchased.

Coverage B (Other Structures): will cover damage to the detached structures of your home such as fences, outdoor kitchens and bars, sheds, pools, guest houses, and detached garages. When determining your coverage B limits, it is important you survey your property and determine how many “other structures” you have, their material type, and an average idea of what it would cost to replace them should the unexpected occur

Coverage C (Personal Property Insurance): will cover your personal items inside your home. Usually, it defaults to 25% of the Coverage A limit and may be increased to 75% (aka the cost to rebuild your home at today’s prices is $100,000 so your personal property insurance would cover up to $25,000 of the contents of your home).

Coverage D (Loss of Use Coverage): covers living expenses should your home be deemed unlivable/uninhabitable due to a covered loss. Coverage D defaults to 10% of Coverage A and cannot be excluded.

Coverage E (Personal Liability Coverage): provides protection of personal finances should someone become accidentally injured in your home and file a lawsuit against you and your property. Coverage is offered with a standard $100,000 limit but may be increased up to $400,000.

Let’s Bring it Home- One more time! Head, Shoulders, Knees, and Toes.

Each insurance policy and insurance carrier offers different limits on their coverage. It is important you understand what is covered within your homeowners insurance policy. We encourage you to review your current home insurance policy, survey your property, and contact your agent should you have any questions or need to make any changes. Florida Peninsula is also here to help our policyholders, for more information, or to get a quote, please call 877-229-2244